Line 14 Codes and Line 15

Before you can fill out the 1095-C, you’ll need to determine which codes apply to the insurance plan(s) that your company has offered employees. A “Code Series 1” code is entered in each month of the calendar year to describe the offer of coverage made to employees. These codes describe the type of coverage offered (whether it offers minimum value and/or minimum essential coverage), who it is offered to, and for the first code, what affordability safe harbor was used to determine affordability (there are three different safe harbors).

If you are not sure which code to use after reviewing the 1095-C instructions, check with your insurance company, to verify whether the plan(s) you offered provided minimum value (MV) and minimum essential coverage (MEC). We cannot help you with this, so don’t ask us what line 14 code you are supposed to use!

You should know whether you are offering the coverage to the employee only, employee and dependents, employee and spouse, or employee, spouse and dependents.

The final piece of information you need to know is your affordability safe harbor. You do remember what affordability safe harbor you used, right?

In case you forgot (or never knew!) this is the method that you used to determine whether or not the employee’s share of the premiums was affordable. There are three methods:

- 9.5% of mainland single federal poverty line (MSFPL)

- Form W-2

- Rate of pay

If you are covering the entire cost of the insurance, then the employee doesn’t have any cost, and the affordability safe harbor is not particularly relevant, but you still must pick one.

If you are basing the employee contribution on a percentage of gross wages, the Form W-2 safe harbor could apply. The percentage that the employee contributes must be 9.5% or less.

The Rate of pay safe harbor may be a relatively easy calculation to perform that would apply to all employees. Using this calculation, you would multiply $9.00/hour (minimum wage) by 130 hours/month. This gives you the minimum wage that any employee would need to have before qualifying for coverage of $1,170/month. Taking 9.5% of that total gives you $111.15. As long as the employee’s contribution is less than this, the insurance can be considered affordable.

(Of course, the affordability calculation could be done with each employee’s individual hourly pay rate. Using the minimum wage calculation provides you with a cap on employee contributions that could be used across the board for all employees.)

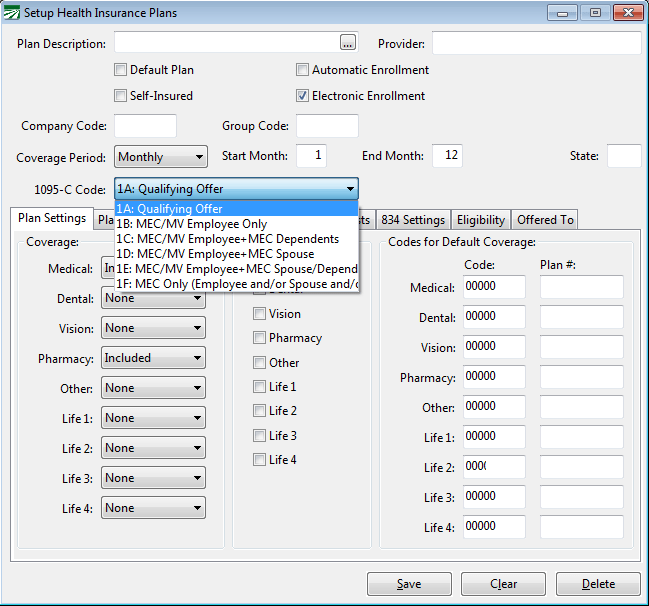

Between these three pieces of information, you should be able to determine which code to use. Each plan that you have set up should have a code assigned to it from one of the following:

Code 1A applies if the insurance coverage you offer includes MEC and MV, was offered to the employee, spouse and dependents, and you use the MSFPL safe harbor.

Code 1E applies if the insurance coverage you offer includes MEC and MV, was offered to the employee, spouse and dependents, and you used either the W-2 or Rate of Pay safe harbors.

Codes 1B, 1C, 1D apply when the coverage is not offered to either the spouse and/or dependents.

Code 1F would apply to a plan that provides MEC but not MV.

When code 1A is used, it is not necessary to report any amounts on line 15. When one of the other codes is used (1B, 1C, 1D, 1E, 1F) then you must report the amount of the employees contribution for each month on the 1095-C. This program will use the Employee Share for Self Only coverage to report this amount. (Of course this should already be a part of your plan setup for the employee deductions to be calculated.)

If your plan is age rated, then this amount will vary for each employee depending on their age. To handle this, an Age Rated Costs tab page has been added to the Health Insurance Plan setup window where this amount can be entered for each age range that applies to your policy. The payroll program will also use the Age Rated Table to determine the cost for the employer sponsored health coverage amount (DD code on the W-2). A future update will also use the Age Rated Plan table in determining the employee’s deduction.